now loading...

Earlier this year, predictions that a recession would soon grip the global economy were rampant. But, more than halfway through 2023, China is the only major economy that appears to be at significant risk of a prolonged slump. In New York and London, and across Europe, stock markets are soaring. In Tokyo, the Nikkei hit a 33-year high in June. While some economies are struggling, a global recession now appears highly unlikely.

An economic downturn can have many causes. For example, excessive consumer and investor confidence or very high levels of public spending can drive up aggregate demand to the point that inflation begins to rise, forcing policymakers, especially central banks, to intervene to cool an overheating economy. If they overdo it – say, by raising interest rates, and thus borrowing costs, too aggressively – they can push the economy into recession.

A recession can also arise from the supply side. When a particular sector or the economy as a whole is booming, suppliers ramp up production. But if demand begins to fall, supply can begin to build up, hampering and even halting growth.

Neither of these factors is in play today: though the US Federal Reserve and the European Central Bank have been pursuing monetary tightening, demand has not collapsed, and supply is not piling up. Instead, recent recession forecasts were derived largely from statistical analyses of past data – analyses that did not adequately account for the impact and legacy of the Covid-19 pandemic.

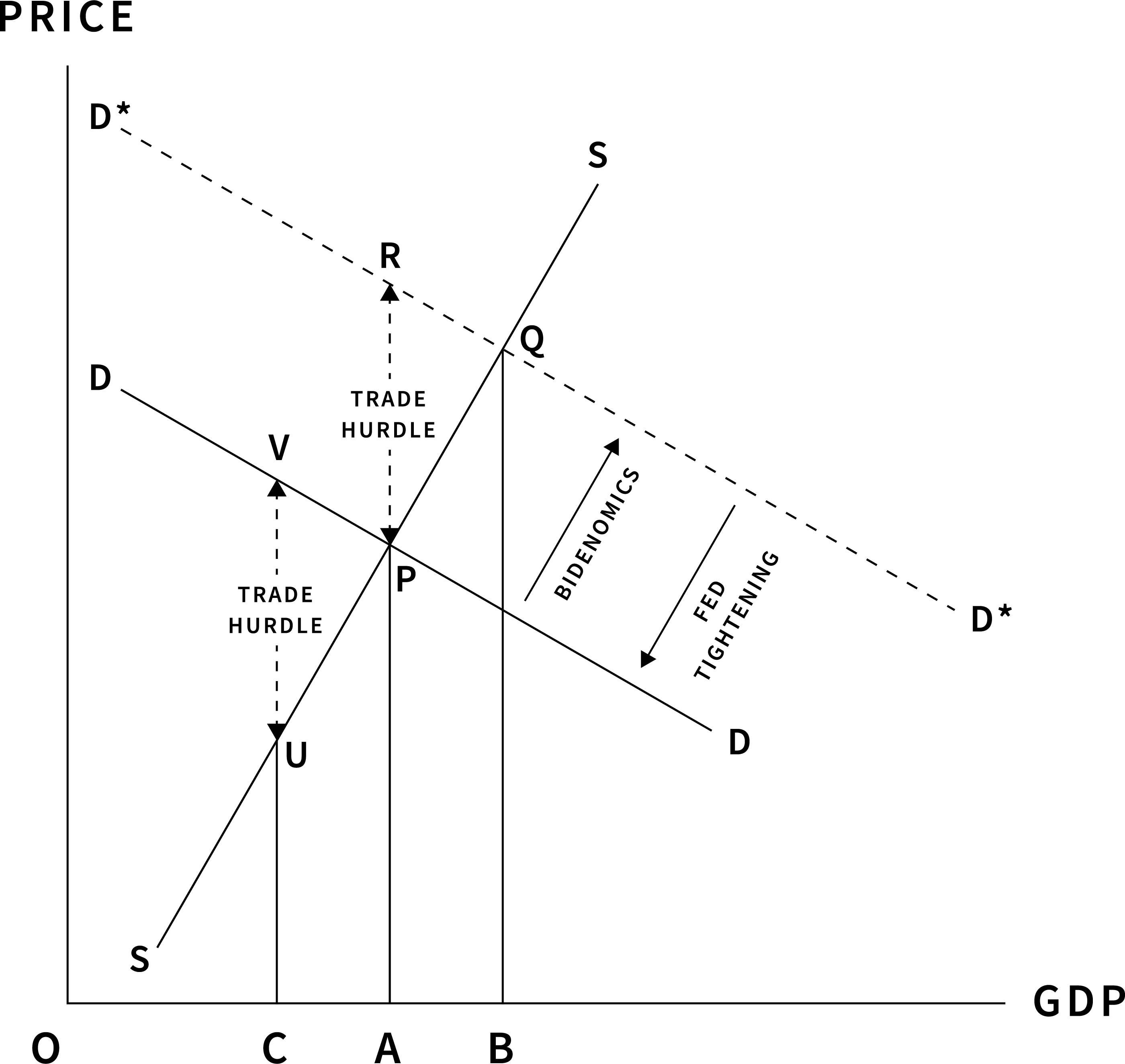

Figure 1 offers a simple depiction of the effect of the pandemic on a national economy. Under normal circumstances, the intersection ( P ) of aggregate supply ( SS ) and aggregate demand ( DD ) determines the equilibrium price ( AP ) and traded volume ( OA ), which can be interpreted as the aggregate output. Demand inflation is triggered by the rightward movement of the demand curve, and cost-push inflation is brought about by the upward movement of the supply curve.

But the movement of the SS and DD curves fails to capture a key feature of the pandemic: trade was highly desirable, on both the supply and demand sides, but less safe. People wanted to dine out, and restaurants wanted to serve them. But neither could do so – at least not to the same extent as usual – because of pandemic risks and restrictions. The same goes for countless other activities and industries, from travel to in-person meetings with business partners and service providers.

So, the pandemic did not create an imbalance between supply and demand so much as a disconnect, which forced buyers and sellers to incur extra costs, from wearing masks to moving dining tables farther apart, to make their exchanges possible. These barriers – captured in Figure 1 by the vertical distance between the curves – meant that actual output was no longer determined only by the intersection between the DD and SS curves; the size of the trade hurdles also mattered. The higher the barriers, the greater the distance between the DD and SS curves, and the bigger the decline in output.

This drop in output triggered powerful policy responses. In the United States, for example, President Donald Trump’s administration launched a massive stimulus package, augmented by his successor, Joe Biden, to boost demand – that is, shift the demand curve rightward. The trade hurdles were still there, but the adjusted position of the demand curve ( D*D* ) meant that they no longer dragged output far below normal, or pre-pandemic, levels. Indeed, thanks to so-called Bidenomics, US output returned approximately to its original equilibrium point.

When pandemic restrictions were lifted, the “wedge” created by trade hurdles was eliminated. But the demand curve remained in its adjusted ( D*D* ) position. The supply and demand curves thus intersected at a higher equilibrium point ( Q ), implying more output and – crucially – higher price levels. The Fed’s tightening has aimed to counteract these effects, by pushing the demand curve closer to its original position ( DD ).

While the Fed’s monetary tightening does increase the risk of a growth slowdown, or even a recession, in the US, recent economic indicators – not least strong employment figures – suggest that a soft landing is perfectly feasible. In fact, both the Biden administration’s demand-boosting policies and the Fed’s inflation-cooling interventions were entirely appropriate.

Perhaps more important, by strengthening the US dollar, higher US interest rates stimulate other economies’ exports. This makes the kind of global recession that so many predicted even less likely.

Koichi Hamada is a professor emeritus at Yale University and a special adviser to former Japanese Prime Minister Abe Shinzō.

Copyright: Project Syndicate