now loading...

Many experts believe that the US dollar’s global hegemony, which has endured for nearly 80 years, is finally coming to an end. This outcome is not impossible: economic crises, increased domestic polarization, and strong geopolitical headwinds could indeed culminate in the currency’s meltdown. But it is not likely.

Debates about the future of the international monetary system often fail to appreciate the greenback’s full-spectrum dominance, which requires understanding its role in public and private markets, as well as the various incentives to hold dollars. So long as self-reinforcing synergies and forms of opportunism continue to prevail, narrowing the yawning chasm between the dollar and other currencies will remain difficult.

To be sure, there are threats to dollar supremacy. The greenback’s primacy and pervasiveness in the global financial system has become a major bone of contention in the great-power struggle between the United States, China and Russia. These geopolitical challenges are happening against a backdrop of high interest rates and America’s polarized politics, which prompted the drawn-out negotiations over the US debt ceiling earlier this year; taken together, they risk undermining the perceived safety of dollar assets. But for the greenback to be unseated, multiple actors must support a substantial currency shift.

Moreover, the US – and potentially other countries – have a vested interest in preserving the dollar’s status as the world’s only truly global currency. Americans benefit from the ease and convenience of transacting in dollars, seigniorage, monetary flexibility, and being the world’s safe haven in times of crisis. For the US government, it serves as a non-military instrument of coercion with which to police the world, as well as a source of prestige.

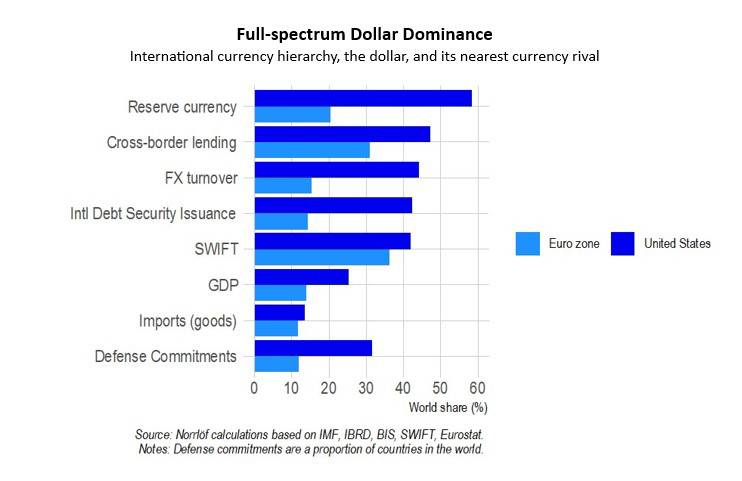

Measuring dollar dominance requires a closer look at the many functions – from medium of exchange to unit of account and store of value – the greenback serves outside the US. Governments and monetary authorities use the dollar to intervene in foreign-exchange markets, to hold official reserves, and as a pegging currency. Private actors, meanwhile, rely on it as a vehicle currency, for invoicing and settlement of trade, and for investment purposes. The interplay between these different actors and roles has propelled the currency to its hegemonic position, as shown in the figure below.

The dollar outperforms its main rival – the euro – by the largest margin in the role of reserve currency, which foreign governments and monetary authorities use as an exchange-rate peg or for interventions. Government decisions thus matter for the dollar’s continued primacy. Official entities could coordinate foreign-exchange interventions to prop up or hold down the dollar. But that would require collective action, as would the successful implementation of alternative payment systems and liquidity arrangements, such as China’s Cross-Border Interbank Payment System ( Cips ), a renminbi-based rival to the US Clearing House Interbank Payments System ( Chips ), or the proposed joint reserve currency issued by the Brics group of major emerging economies. The question is whether such coordination is possible.

In the post-Cold War era, governments have been motivated primarily by economic factors when deciding whether to bulk up on a foreign currency. The liquidity, depth, and breadth of the dollar market has made the greenback widely accessible and cheaper to use than alternatives. Feedback loops between official institutions and private actors have also encouraged governments and monetary authorities to accumulate dollar-denominated reserves. For example, in times of crisis, private actors rely on central banks to supply them with dollar assets, sometimes via swap lines extended by the US Federal Reserve.

Private actors’ willingness to use and hold dollars is also a choice based on economic considerations: these actors are likely to settle payments – and thus store value – in the invoicing currency. But they coexist within a decentralized system in which each typically accounts for a small slice of the pie. Even the considerable dollar assets held within large financial institutions comprise deposits by separate entities without the means or incentives to act collectively. Thus, while independent decisions could chip away at the dollar’s global standing, a deliberate and coordinated private effort to subvert the current system is highly unlikely.

To bring about a dollar collapse and forge a new world order in which the greenback plays a diminished role would require all users to break these network effects and suffer the consequences. Governments would need to sever economic and political ties to the US. To fulfil the Brics’ pledge to create an alternative reserve currency and payment system, for example, many of its members would have to stop relying on US liquidity and consumer demand.

Such initiatives depend on the participation of major economic actors or a preponderance of minor ones. It is unlikely that the major economies would come on board, because, with the exception of China, they all enjoy access to dollar-swap lines. Moreover, if governments abandon the dollar before another currency becomes dominant, they risk losing a liquidity lifeline in times of crisis. Many small actors would likewise be loath to jump ship, given that opportunism largely precludes collective action.

Apart from any direct economic costs, governments that conspire to thwart the dollar system risk losing America’s security guarantee. Even countries that do not benefit directly from US defence commitments will probably be reluctant to land on the wrong side of such a formidable military power.

Positive feedback across the greenback’s official and private functions, the network effects associated with its incumbency advantage, and opportunism discourage collective action against the status quo. For governments, unplugging from the dollar system also means disconnecting from all that the US has to offer, including liquidity provision, consumer demand, dollar-swap lines, and a security umbrella. Currency dominance is sticky. Absent major economic upheaval or a geopolitical realignment, the dollar’s global hegemony will continue to create the conditions for its own persistence.

Carla Norrlöf is a professor of political science at the University of Toronto and a non-resident senior fellow at the Atlantic Council.

Copyright: Project Syndicate